9520 Palatine Avenue N Seattle, WA 98103 Listing price: $639,000

MLS #1982788

Beds: 3

Baths: 2

1,220 sqft

Classic 1940’s bungalow with a bonus room addition that adds surprising space to the typical design for this era. Fir floors, tall ceilings, cheerful sunny rooms, nice garden lot with alley access for easy extra off-street parking. Bonus room has soaring vaulted ceilings and cozy free-standing fireplace, lots of flexible uses:TV rm, Primary bedrm, friendly guest quarters or home business w/ sep entry. Hall stairway leads to finished attic space ideal for storing seasonal decorations, etc. Updated copper plumbing, gas furnace, new hi-end roof in 2012. House is located forward on the lot, future DADU? Walk to Greenwood area restaurants/ shops/brew pubs/parks and Northgate Light Rail approx. 1 mile. Lots of possibilities and upside potential!

Information provided as a courtesy only, buyer to verify. For more, go here.

Becoming a homeowner comes with many responsibilities, but if the home you’re purchasing requires you to be part of a Homeowners Association (HOA), you’ll have to follow additional guidelines and pay additional fees. As you’re looking for homes, talk to your agent about whether purchasing a home that’s part of an HOA is right for you.

What is a Homeowners Association (HOA)?

A Homeowners Association is an organization that governs a community of homes. Homeowners within the governed community must follow certain guidelines for property upkeep and maintenance and will face restrictions on their ability to make additions and/or changes to the property. These rules exist to maintain a standard level of quality amongst the community to maximize property value.

Different HOAs may have different stipulations based on the type of housing they govern. For example, an HOA may oversee a community of detached single-family homes, but they are commonly found in communities of condo or townhome housing styles where there is a shared, communal living style. Each HOA has a Board of Directors in charge of enforcing rules, collecting fees, and managing the funds, and certain associations may hire a third-party management company to help the Board of Directors carry out their operations. The members of an HOA are the residents who live in that community. Here are some examples of typical HOA property restrictions:

Exterior paint color choices must be submitted for approval

Grass must be mowed regularly

Flower beds must be kept weed-free

Noise regulations and/or noise curfew

Pet restrictions (type of animal and/or number of pets per household)

Homeowners Association (HOA) Pros and Cons

Living in an HOA community means your property will maintain its curb appeal and you can live with the knowledge that systems are in place to protect property values. However, the benefits come with additional restrictions on your freedoms as a homeowner while increasing your monthly payments.

If you buy in a development governed by a Homeowners Association, you will be required to pay HOA fees on top of your monthly mortgage payment. Typically paid monthly, HOA fees go toward the neighborhood’s shared spaces, property maintenance, and amenities. Homeowners Association fees vary greatly depending on the particulars of that community’s agreement. These fees often cover landscaping costs, parking, community security, garbage pickup, maintenance and repair, insurance, and other amenities, such as a shared pool or gym. If the home is your primary residence, your HOA fees are not tax-deductible.

HOA fees are an additional expense you’ll have to budget for when buying a home. To get an idea of what you can afford, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price, accounting for any HOA fees you may incur.

Interior design solutions come in all shapes and sizes. After all your furniture items, art, and other physical items are all in their right place, decorating with house plants can provide the perfect final touch. The best plants for your home are the ones that will thrive in your local climate while complementing your existing décor. Here are a few common house plants and their corresponding interior design styles to aid your decorating efforts.

Decorating with House Plants to Match Your Décor Style

Mid-Century Modern

Mid-century modern interior design is ubiquitous, and for good reason. Its simple concepts, open spacing, and emphasis on natural elements make it one of the premier interior design styles for homeowners and design experts alike. A Split-Leaf Philodendron, or “Swiss cheese plant,” is ideally suited for these interior spaces, and its signature leaf holes make it a visual focal point. Swiss cheese plants will thrive in open spaces with access to natural light, climbing toward the ceiling as space allows. For the same reasons, Fiddle-Leaf Figs feel at home in a mid-century modern aesthetic.

There’s an inherent give and take with industrial interior design in that it foregoes traditional elements that we associate with comfort for stylistic choices that create a strict-yet-visually appealing environment. Decorating with house plants can add vibrance to an industrial backdrop of wood, steel, brick, stone, and copper without compromising the edginess of the style. Both Snake Plants and Cast Iron Plants will harmonize with an Industrial space. Both are low-maintenance plants that mesh well with materials that evoke toughness and durability.

Minimalist

The combination of minimalism and house plants is a match made in heaven. Given minimalism’s focus on the reduction of waste and clutter and the importance of bringing the outdoors in, all signs point toward decorating with house plants. Being selective about which plants you include will keep everything in line with the fundamental concepts of minimalism—too many plants and things would easily feel off balance. Large-leaf plants are a perfect solution for minimalist decorators, such as Rubber Plants, Bird of Paradise, and Silver Evergreen.

The Farmhouse interior style prioritizes cleanliness and an inviting spirit. Its white-washed backdrop of whites, grays, and beiges makes it a fitting canvas for the lush green additions that a selection of house plants can provide. Spider Plants work well to fill shelf space, which come in both solid green and white-striped varieties. These plants are easy to take care of and thrive in partial sun or shade. Aloe Vera plants in the kitchen can refresh the look of your shelving or counter space.

Homeowners with traditionally styled interiors have a whole host of options to choose from. Any classic plant species will complement its traditional surroundings, but more specific choices can bring out the uniqueness in your home. If your decorations are rife with patterns and geometric shapes, perhaps a fern or Amazon Lily would help to balance the room. Bamboo may be a natural fit for your home depending on your existing décor. If you’re looking for a hanging display to fill empty wall space, consider Devil’s Ivy.

As always, research the watering and sunlight needs of a house plant before bringing it into your home. For more on decorating with house plants, be sure to read our room-by-room guide:

The math of a home sale is relatively straightforward. Sellers list their home at a certain price, a buyer makes an offer, and eventually the two parties reach a final, agreed-upon price. However, between these two points in the selling process, there are several other figures that go into to setting a home’s value that you should be aware of. Your real estate agent will be your best resource in interpreting the different values associated with your home and what they mean as you prepare to sell.

Understanding the Value of Your Home

Listed Price (Asking Price)

Also known as an asking price, the listing price of a home is the price at which a seller lists their property when it goes on the market. The listing price is a gross price, meaning the costs associated with selling the home are not included. A real estate agent’s Comparative Market Analysis (CMA) will accurately set your home’s listing price, accounting for the various factors that influence home prices including location, condition, seasonality, local market conditions, and more.

The listing price is a starting point for negotiations with buyers. You may receive an offer that matches your asking price, but it’s common for buyers to make offers at other price points. You can either accept, reject, or make a counteroffer in response until you and the buyer reach an agreement.

Whether you’re selling in a buyer’s market or a seller’s market may determine you and your agent’s approach to the listing price of your home. There may be certain pricing tactics you can employ to either drive buyer attention or increase competition, but if your home’s listing price strays too far from its market value (see below), it could stay on the market for longer than you expected.

Market Value

As a seller, you’re interested in what buyers are willing to pay for your home. By taking into account a home’s condition, size, curb appeal, and features, as well as local market conditions and what comparable homes are selling for, a home’s market value reflects the price buyers will pay for a property.

Appraised Value

A home’s appraised value is determined by a professional appraiser to ensure that the lender is loaning the correct amount of money for the home. Appraisers assess the home’s layout and features, square footage, gross living area (GLA), overall condition inside and out, home updates and remodels, and more. If the appraised value comes in too low or too high, the buyer and seller must renegotiate for the deal to go through. In competitive markets, buyers may include an appraisal gap guarantee in their offer, which states that the buyer will cover the difference between the price of the home and the appraised value.

Sale Price (Purchase Price)

Also known as the purchase price, your home’s sale price is what it ultimately ends up selling for. Once you and the buyer have reached an agreement on the terms of the transaction, the buyer will have the home inspected and final negotiations may occur based on the findings of the inspection. Familiarize yourself with the Common Real Estate Contingencies buyers may include in their offer and what they mean when selling your home.

Net Proceeds

So, how much do you actually make on the sale of your home? After subtracting the total costs of selling from your home’s sale price, you’ll arrive at your net proceeds. This is the amount you walk away with from the transaction.

Assessed Value

Your agent’s CMA is a reliable method of determining your home’s value for its eventual sale, but its assessed value is used for taxation purposes. Employed by local municipal or county entities, an assessor will conduct a review of your property to determine its assessed value. The assessor’s findings are passed to local tax officials, who use that number to calculate the home’s property taxes.

Featured Image Source: Getty Images – Image Credit: kupicoo

This video is the latest in our Monday with Matthew series with Windermere Chief Economist Matthew Gardner. Each month, he analyzes the most up-to-date U.S. housing data to keep you well-informed about what’s going on in the real estate market.

Hello there, I’m Windermere’s Chief Economist Matthew Gardner and welcome to this month’s episode of Monday with Matthew. You know, one of the many things I love about being an economist is that it is a remarkably humbling profession. You see, just when we start to believe that our models are close to perfection, something comes along to remind us that forecasting isn’t an exact science.

And if you’re wondering what I am talking about, I recently took a look at the 2022 mortgage rate forecast I put out at the start of the year and…well, let’s say that rates rose at a far faster pace than I had anticipated. I thought that now would be a good time to take another look at rates and share my thoughts on the direction that they will likely take during the rest of the year and my reasoning behind it. And that means we need to talk about inflation.

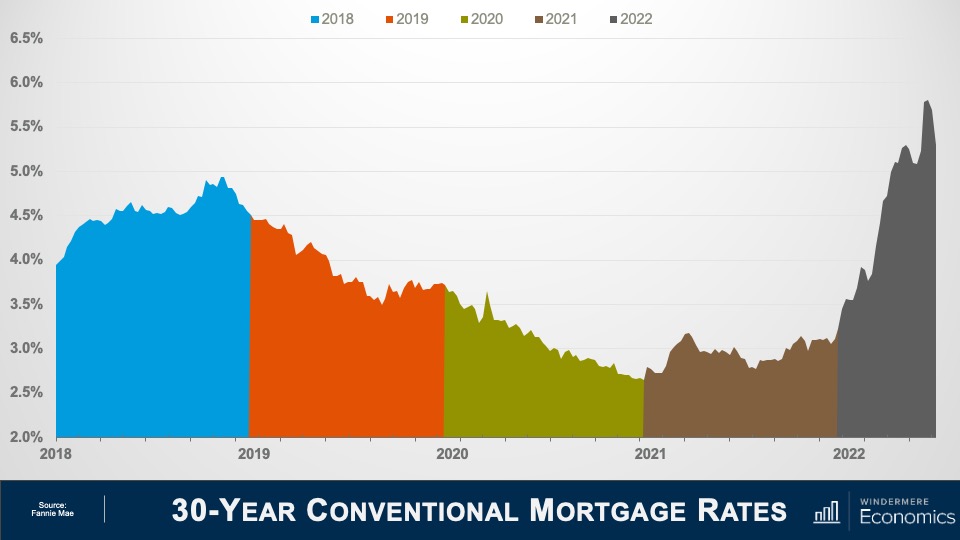

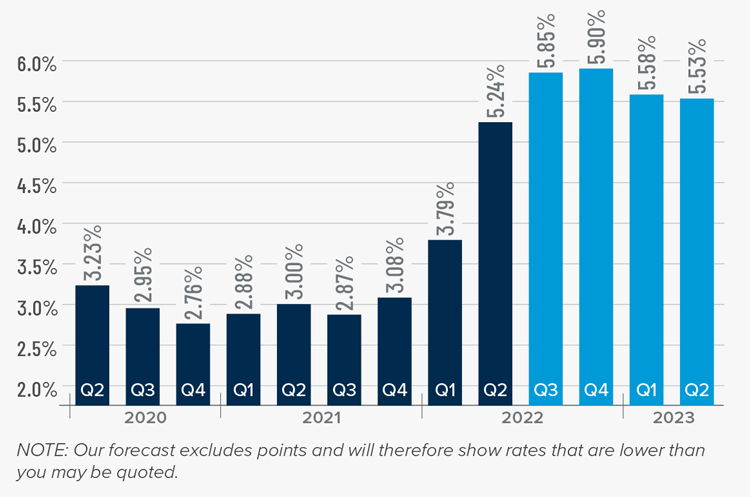

30-Year Conventional Mortgage Rates: 2018 – 2022

So, a quick look back. As you can see, there wasn’t much to celebrate in 2018, with rates rising from 3.95% to 4.94% before pulling back and ending the year at around 4.5%. In 2019, rates fell following the Feds’ announcement that they were likely done with raising the Fed Funds Rate, and the mortgage market also reacted positively to the announcement from the White House that they were going to impose tariffs on select Chinese imported goods. We saw an uptick in late summer, but that was mainly due to news related to BREXIT.

In 2020, rates were dropping but spiked very briefly when COVID-19 shut the country down and bond markets panicked. But with the Fed jumping in with an emergency rate cut and announcing that they would start buying a significant number of treasuries and mortgage-backed securities, rates tumbled to an all-time low of just 2.66%. In 2021, rates rose as new COVID infections plummeted, but then dropped again as the Delta variant took hold, but ultimately trended modestly higher in the second half of the year.

And then we get to 2022. Rates started the year at just over 3.1% but have since skyrocketed to over 5.8% before a small pullback that started a few weeks ago. In as much as economists expected rates to rise this year, nobody anticipated how fast they would rise. So, what went wrong? Well, there’s actually a rather simple answer.

Even though we expected rates to trend higher in 2022, there were two things we hadn’t built into our forecast models.

Russia’s invasion of the Ukraine

Inflation continued to climb for far longer than we expected

So, how do things look for the rest of the year? To explain my thinking, it’s important to remember that the bond market and, by implication, mortgage rates hate nothing more than high inflation because when inflation is running hot, it limits demand for bonds which, in turn, forces the interest rate payable on bonds to rise and this pushes mortgage rates higher.

But what’s been fascinating to watch is that over the past couple of weeks, rates have actually been dropping which is certainly counterintuitive given where inflation is today. And the only reason I can see for this is that bond traders were thinking that inflation might be topping out.

But then we got the June CPI numbers, and it certainly didn’t suggest that inflation was slowing, in fact it showed the opposite. But even though the total inflation rate hasn’t yet peaked, I believe that a shift has actually started and that we are closer to a peak in inflation than you may think.

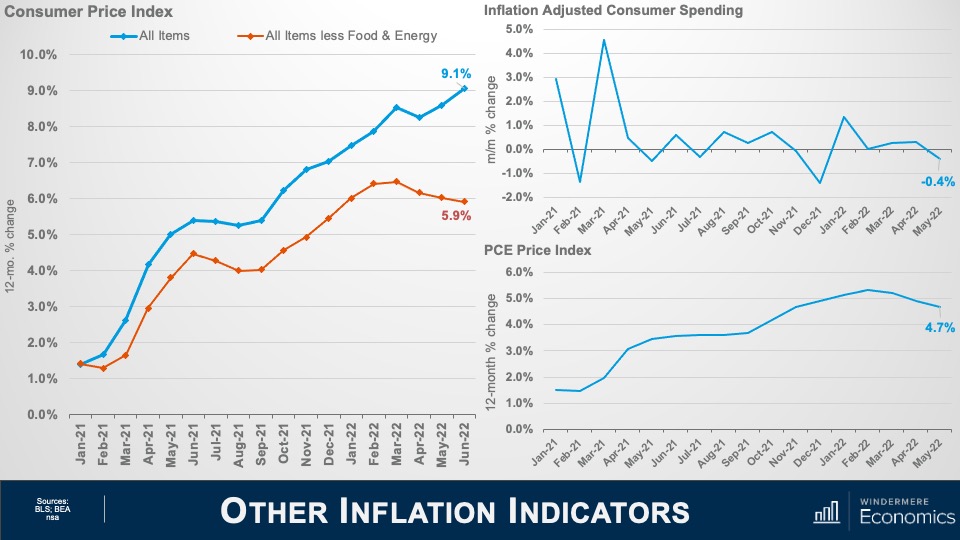

Indicators of Inflation: Consumer Spending

The June CPI report showed the headline inflation rate still trending higher but look at the core rate which excludes the volatile food & energy sectors. That has actually been pulling back for the past three months. And consumer spending when adjusted for inflation fell 0.4% in May. That’s the first monthly drop since last December, and I expect the June number when it comes out at the end of the month to show spending dropping even further.

This is a very important dataset that often gets overlooked but it is starting to tell me that the economy is slowing because of inflation and slower spending acts as a headwind to further price increases.

The core PCE price index is up 4.7% year-over-year, but this was the smallest annual increase since last November and you can see that it is also starting to roll over. This index is actually the Fed’s favored measure of inflation as it’s more comprehensive that the CPI number as it measures the change in spending for all consumers, not just urban households.

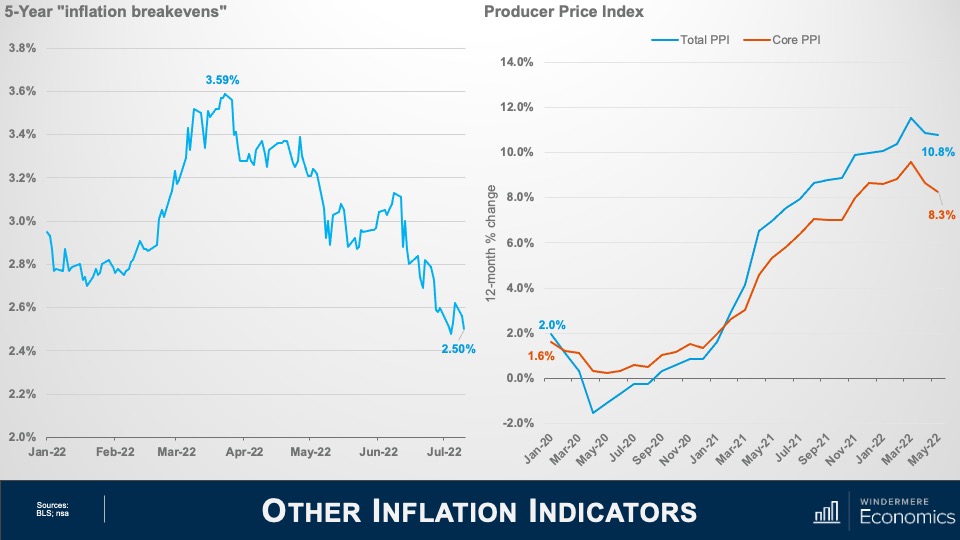

Indicators of Inflation: 5-Year Breakevens and Producer Price Index

The five-year “inflation breakeven” has plunged more than a full percentage point since peaking at just under 3.6% in late March. And this number is important as it lets us know where bond traders expect the average inflation rate to be over the next five years.

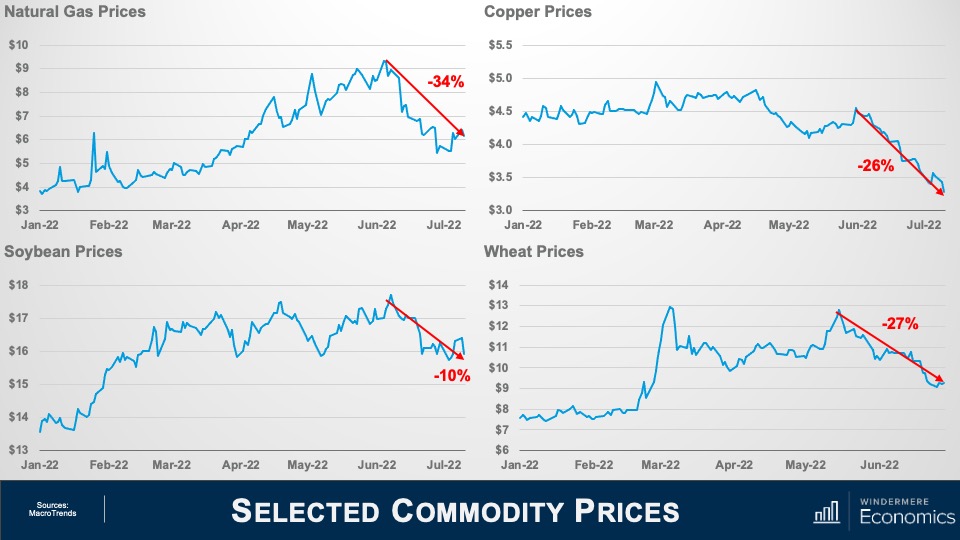

The Producer Price Index measures inflation at the wholesale, not retail, level and even though the total rate rose as energy costs continue to impact the manufacturing sector, the core rate has been pulling back for the past three months. Now let’s look at some commodity prices and see what’s going on there.

The price for natural gas is down over 34% from its recent high

Copper prices are down 26% from the recent June peak and down substantially from March

Soybean prices are down 10%

Despite the war in Ukraine, wheat prices are down 27% from June

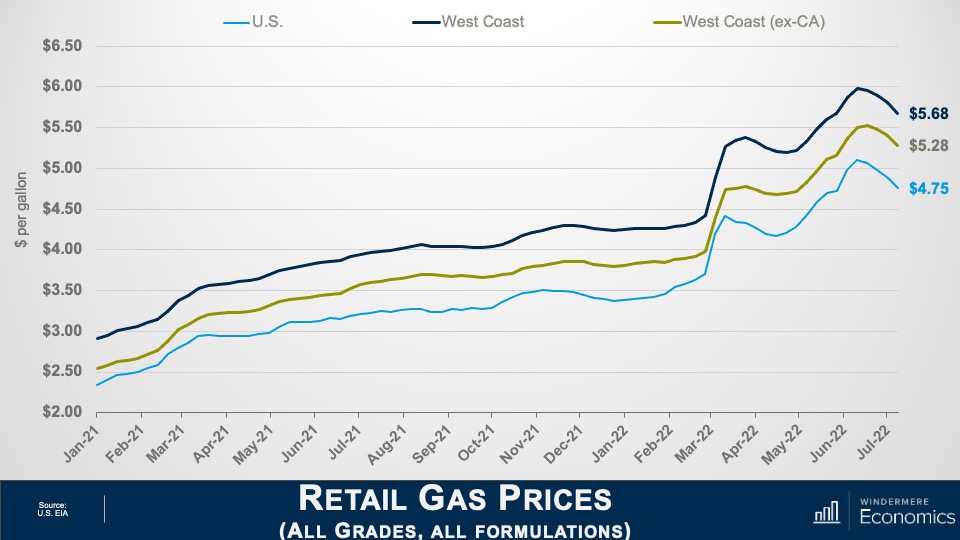

Retail Gas Prices: West Coast, West Coast Excluding CA, U.S.

It appears as if gas prices have also rolled over. Of course, here on the West Coast it’s more expensive than the nation even when you take California out of the equation.

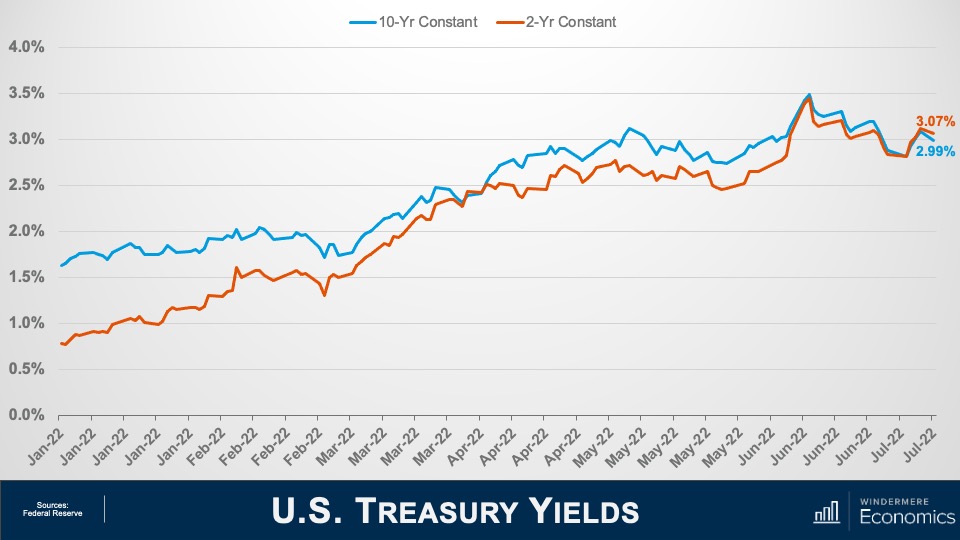

U.S. Treasury Yields: 10-Year and 2-Year Constant

And finally, to cap things off, traders must also be pondering the same numbers as I am because bond yields themselves have been tumbling at both the long and short ends of the yield curve with the 10-year note still yielding less than 3% even after the CPI report and two-year yields, while still elevated, are still down from 2.42% just two weeks ago.

So, given all the charts we have looked at, I hope that you too are seeing some light at the end of the tunnel when it comes to the likelihood that inflation is about to start easing.

No doubt, the headline inflation number for June wasn’t one that anyone wanted to see but, if the trends we have looked at continue, I still expect inflation to start slowly creeping lower, which will push bond prices higher, yields will start to pause—if not drop—and that will allow mortgage rates to hold at or close to their current levels for the time being. Although we could see rates coming down, though they will still start with a five for the foreseeable future. I hope that you have found my thoughts of interest.

As always, if you have any questions or comments about this particular topic, please do reach out to me but, in the meantime, stay safe out there. I look forward to visiting with you all again next month.

Bye now.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

In a seller’s market, many buyers are competing for a limited number of homes. This creates fierce competition amongst buyers and ideal selling conditions for sellers. Sellers will commonly receive multiple offers for their home, often over their original asking price. As the offers stack up, bidding wars will ensue, since only one buyer can ultimately win.

So, how can a buyer rise to the top in these highly competitive situations? First and foremost, it’s important to work closely with your agent to discuss your strategy when buying in a seller’s market. If you find yourself in a bidding war, the following methods may help you secure the home you’re after.

How to Win a Bidding War When Buying a House

Get Pre-Approved for a Loan

Not only is getting pre-approved for a mortgage an important step early on in the buying process, but it’s also a prerequisite for having your offer considered in a bidding war. Without pre-approval, your offer is likely to fall to the bottom of the stack of offers the seller is considering if not tossed aside entirely. Pre-approval gives you credibility as a buyer. It shows that, should your offer be accepted, you have the necessary financing in place to successfully purchase the home. This assurance is key to sellers prioritizing your offer. Pre-approval also helps to speed up the closing process, allowing you to move swiftly through mortgage approval and onto other steps to finalize the transaction, such as the home appraisal and home inspection.

Put More Money Down or Pay Cash

Putting more money down on your offer is one way to differentiate yourself during a bidding war. This may be just what sellers are looking for to put one offer over the top of the others. If you’re able to make an all-cash offer—meaning you have the funds available to purchase the house in a liquid account—you stand to seriously strengthen your candidacy. Because an all-cash buyer can make the purchase without having to go through the process of securing a home loan, it streamlines the buying process, reduces risk, and may persuade the seller to select their offer.

Be Flexible About the Inspection and Your Contingencies

In highly competitive markets, buyers are more likely to waive contingencies to sweeten their offer. So, if you find yourself in a bidding war, you may have to consider doing so to keep up with your competition. If you’re buying and selling a home at the same time, know that making an offer contingent upon the sale of your current home—what is known as a “sale contingency”—won’t be as appealing to sellers during a bidding war, since other buyers will likely be waiving contingencies left and right.

When it comes to the inspection, being lenient can give you a leg up on your fellow bidding war buyers, but it can open you up to added risk as well. Waiving the inspection requirement entirely is an even riskier proposition, as you could end up purchasing a home that needs serious repairs that may not be evident at first glance. When forming your offer strategy with your agent, take time to discuss how you’re willing to modify your inspection requirements.

Escalation Clause

Imagine an auction where multiple buyers are going back and forth, upping each other’s offers. The auctioneer accepts each new price, only for it to be surpassed by the next offer that comes flying in seconds later. This is the essence of an escalation clause in real estate. This clause states that if the seller gets a higher offer, the buyer will raise theirs. The specifics of this clause will spell out how much the buyer is willing to go over the higher bid, as well as their price limit. Including an escalation clause in your offer shows you’re willing to participate in the bidding war, so it’s important to understand what you’re signing up for beforehand. In highly competitive markets, escalation clauses can lead to homes selling for significantly higher than their listing price.

Closing Date Flexibility

Showing that you’re flexible when it comes to the closing date may help put your offer over the top. Remember that the best offer for a seller isn’t just about the price; it’s about which offer removes risk and aligns with their goals. For example, let’s say the seller is in a pinch trying to find a new home. If another buyer’s offer comes in higher than yours, but they are rigid when it comes to the closing date and you’re willing to give the seller more time to find their new home, the seller very well may choose your offer, simply because it works better for them.

Appraisal Gap Guarantee

Sometimes there can be a gap between a home’s appraised value and its purchase price. Many real estate contracts will contain an appraisal contingency, which states that the buyer can back out of the contract. In these situations, an appraisal gap guarantee may be helpful in making your offer stand out. Including an appraisal gap guarantee means that, if there is a gap between the appraised value and the price of the home, the buyer will cover the difference.

For more information on understanding competitive markets and what they mean for both buyers and sellers, read our blog on seller’s markets:

The following analysis of select counties of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere Real Estate agent.

Regional Economic Overview

The most recent employment data (from May) showed that all but 2,800 of the jobs lost during the pandemic have been recovered. More than eight of the counties contained in this report show employment levels higher than they were before COVID-19 hit. The regional unemployment rate fell to 4.5% from 5.2% in March, with total unemployment back to pre-pandemic levels. For the time being, the local economy appears to be in pretty good shape. Though some are suggesting we are about to enter a recession, I am not seeing it in the numbers given rising employment and solid income growth.

Western Washington Home Sales

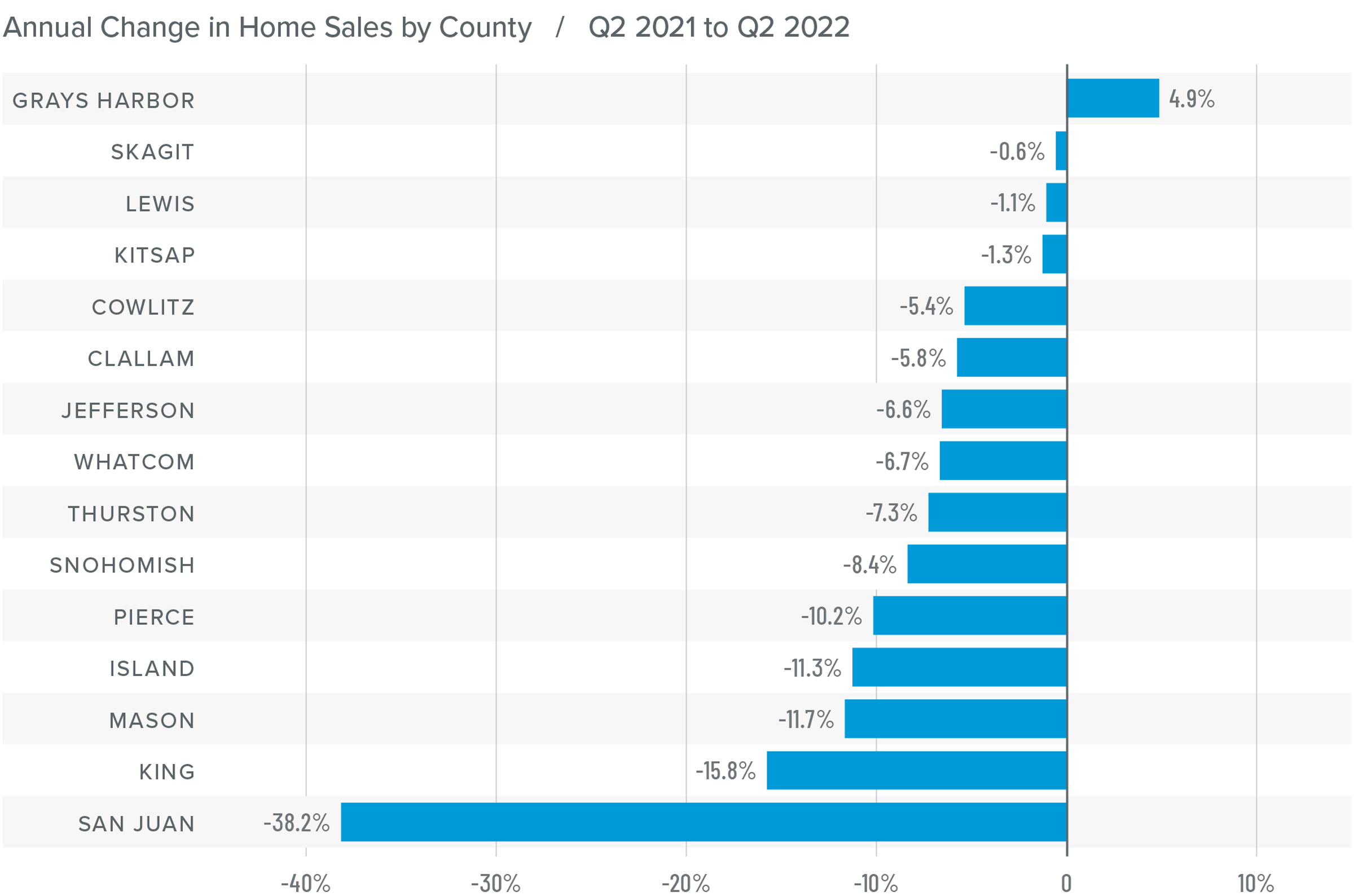

❱ In the second quarter of 2022, 23,005 homes sold, representing a drop of 11% from the same period a year ago, but up by a significant 52% from the first quarter of this year.

❱ Sales rose in Grays Harbor County compared to a year ago but fell across the balance of the region. The spring market, however, was very robust, likely due to growing inventory levels and buyers trying to get ahead of rising mortgage rates.

❱ Second quarter growth in listing activity was palpable: 175% more homes were listed than during the first quarter and 61.98% more than a year ago.

❱ Pending sales outpaced listings by a factor of 3:1. This is down from the prior year but only because of the additional supply that came to market.

Western Washington Home Prices

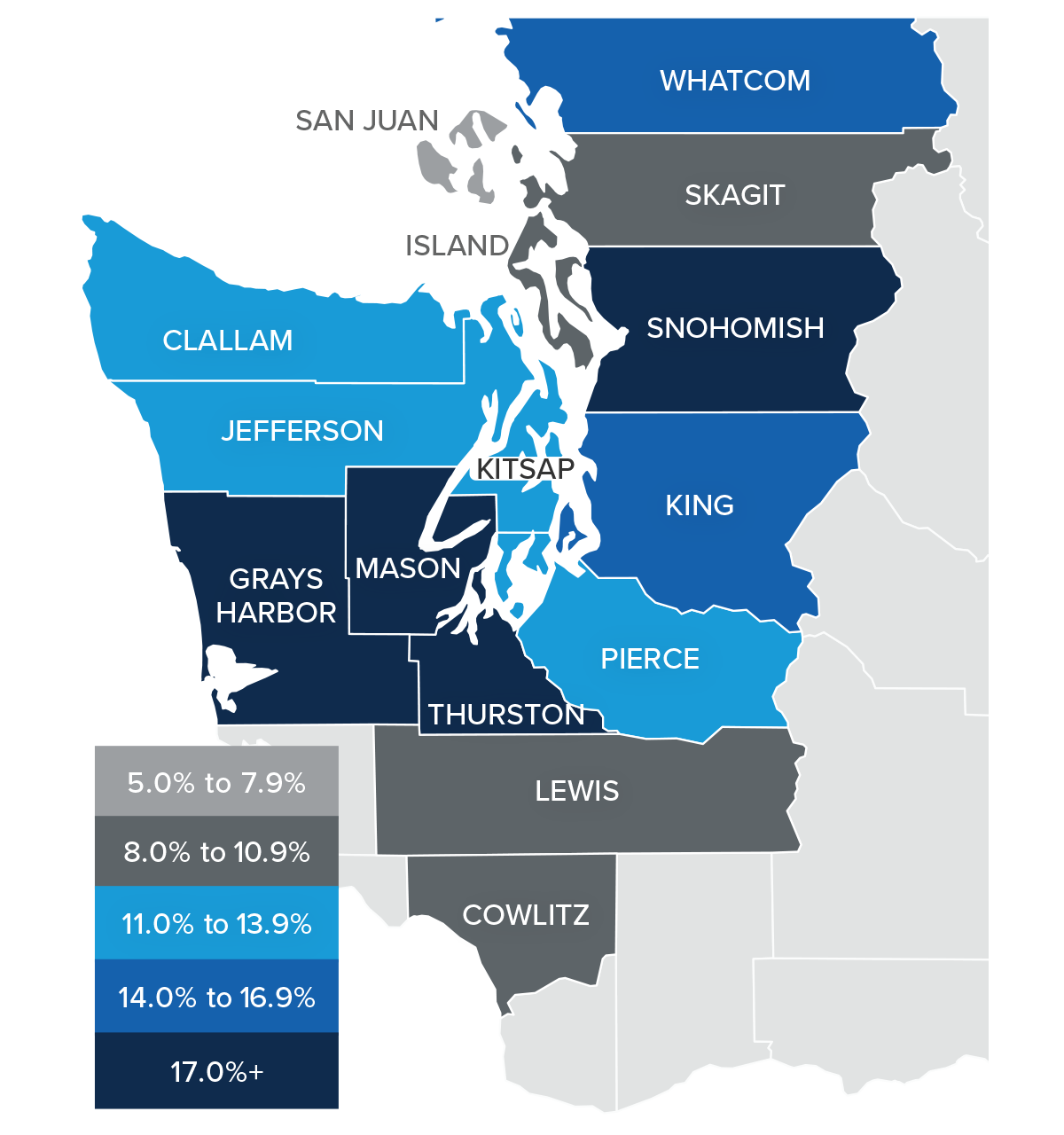

❱ Even in the face of rising mortgage rates, home prices continue to rise at a well-above-average pace, with average prices up 13.3% year over year to $830,941.

❱ I have been watching list prices as they are a leading indicator of the health of the housing market. Thus far, despite rising mortgage rates and inventory levels, sellers remain confident. This is reflected in rising median list prices in all but three counties compared to the previous quarter. They were lower in San Juan, Island, and Jefferson counties.

❱ Prices rose by double digits in all but four counties. Snohomish, Grays Harbor, Mason, and Thurston counties saw significant growth.

❱ List prices and supply are both trending higher, but this has yet to slow price growth significantly. I believe we will see the pace of appreciation start to slow, but not yet.

Mortgage Rates

Although mortgage rates did drop in June, the quarterly trend was still moving higher. Inflation—the bane of bonds and, therefore, mortgage rates—has yet to slow, which is putting upward pressure on financing costs.

That said, there are some signs that inflation is starting to soften and if this starts to show in upcoming Consumer Price Index numbers then rates will likely find a ceiling. I am hopeful this will be the case at some point in the third quarter, which is reflected in my forecast.

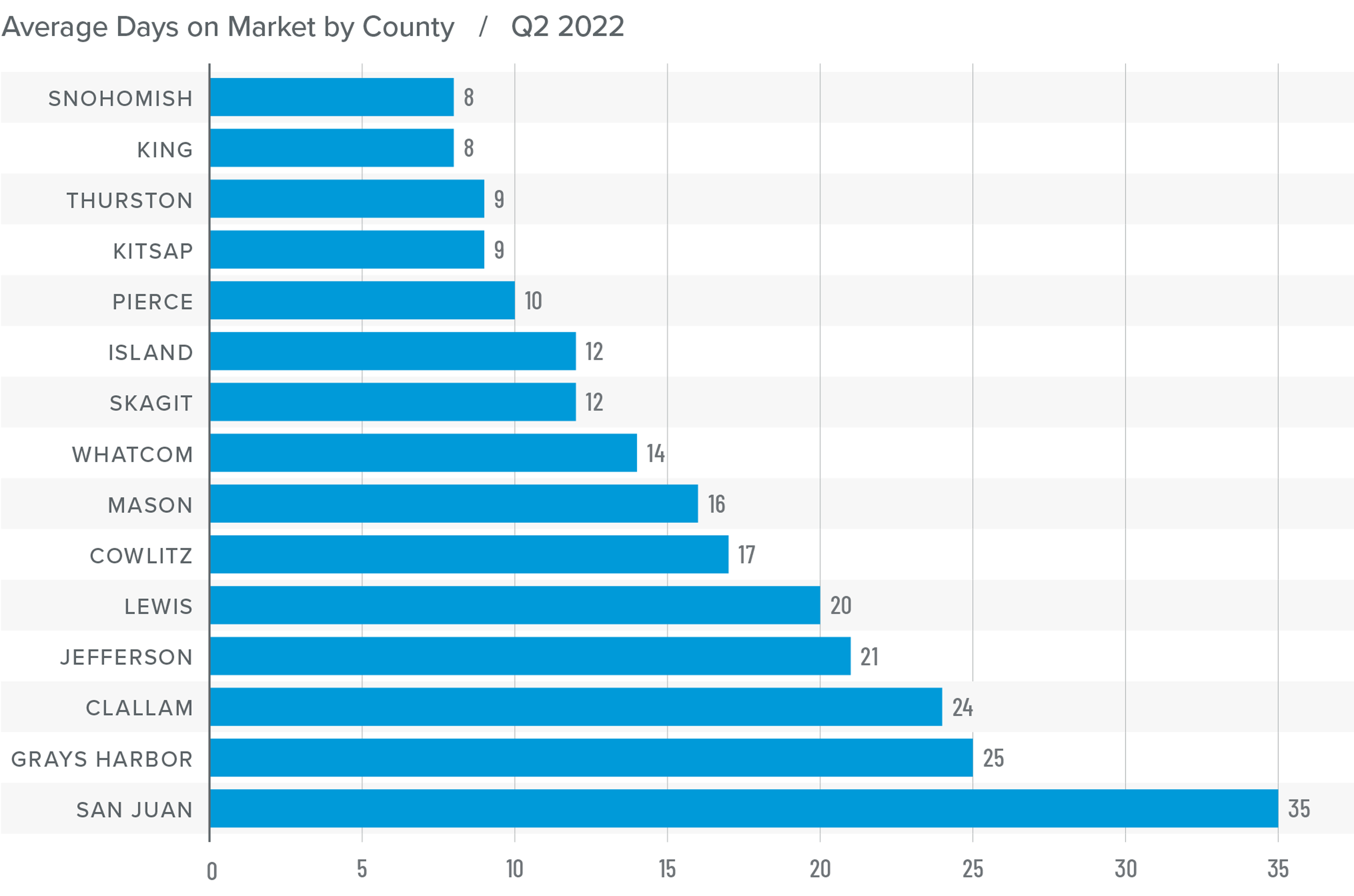

Western Washington Days on Market

❱ It took an average of 16 days for a home to go pending in the second quarter of the year. This was 2 fewer days than in the same quarter of 2021, and 9 fewer days than in the first quarter.

❱ Snohomish, King, and Pierce counties were, again, the tightest markets in Western Washington, with homes taking an average of between 8 and 10 days to sell. Compared to a year ago, average market time dropped the most in San Juan County, where it took 26 fewer days for a seller to find a buyer.

❱ All but six counties saw average time on market drop from the same period a year ago. The markets where it took longer to sell a home saw the length of time increase only marginally.

❱ Compared to the first quarter of this year, average market time fell across the board. Demand remains very strong.

Conclusions

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The economy remains buoyant, which is an important factor when it comes to the regional housing market, particularly as it affects buyers. Even though the number of homes that came to market has jumped significantly, which should favor those looking for a new home, demand is still robust, and the market remains competitive.

Much to the disappointment of buyers, rising listing prices suggest that sellers are clearly still confident even as financing costs continue to increase. While the pace of price growth is slowing, sellers are still generally in control. As such, I have moved the needle a little more in the direction of sellers. Until we see list-price growth and home sales slow significantly, we will not reach a balanced market.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

1125 N 85th Street Seattle, WA 98103 Listing price: $775,000

MLS #:1963619

3,380 SQFT

Lot Size 3,800 SQFT

Taxes: $8,067 (2022)

Type: Multifamily Building

Year Built: 1912

Style: 52 – Duplex

Views: Territorial

This duplex goes from traditional bungalow to urban-edgy in the time it takes to climb a flght of stairs. Entry-level unit maintains the style of the orig. 1912 build:Hardwoods, tall ceilings, picture molding, double-hung casement windows, period millwork, porcelain tile, etc. There is formal dining, large country kitch, 2 spacious bedrms, fantastic office space, and laundry all one level. Top floor unit is 2 stories w/ privt entry, engineered hardwoods, quartz counters, cherry cabinets, bath on each level. 1 bedrm plus xtra finshd space for guest bedrm/office,W/D. Alley leads to 2 covered parking spc + det. gar. Unfinishd 1040sqft. basmt has multi-use/storage potential. LR2 Zoning. Walk to Greenlake/Greenwood amenities, 1mi. to light rail!

Information provided as a courtesy only, buyer to verify. For more, go here.

The mid-century modern movement’s impact on design reaches far and wide. Whether it’s graphic design, architecture, interior design, product development or elsewhere, we see traces of its influence in countless aspects of everyday life today. Mid-century modern homes are known for their signature look and stylistic appeal. Here’s a short guide to understanding the characteristics behind mid-century modern architecture.

Mid-Century Modern Design

Yes, mid-century modern interior design and mid-century modern architecture are two separate things. The interior design style emphasizes clean lines and minimal decoration, the use of natural elements as accents, and a base of neutral colors for decorating. MCM interior design can exist in any type of home regardless of its architectural style, and is often a popular source of inspiration for decorators fond of vintage elements and popular mid-century furniture pieces such as credenzas, teak desks, Eames chairs, etc.

What is Mid-Century Modern Architecture?

Mid-century modern architecture is the exterior counterpart of its interior design branch. Fueled by a massive need for suburban homes throughout the Unites States in the post-World War II era, the stage was set for mid-century modern’s introduction to the masses. Some of the greatest minds in modern architectural history helped develop and proliferate its presence in society, including Ludwig Mies van der Rohe and Frank Lloyd Wright. Though you’ll find unique variations within mid-century modern, there are certain tenets of the architectural style.

Mid-century modern homes have flat roofs with straight lines. This clean geometric approach in roof design is part of a larger philosophical ideal that these homes should blend in with their outdoor environments, thereby working in harmony with nature.

Glass is used heavily, and floor-to-ceiling windows are a common feature, especially in the living room.

The minimalist approach to exterior design is showcased in the easy access to outdoor spaces and the fact that mid-century modern homes are often one-story buildings.

The open spaces created by this architectural style allow for intentional decorating and the use of color splashes to bring energy into them. Mid-century modern interiors often incorporate vibrant, warm colors on top of a calmer, neutral foundation.

For more information on home design, read our guide to industrial design:

This video is the latest in our Monday with Matthew series with Windermere Chief Economist Matthew Gardner. Each month, he analyzes the most up-to-date U.S. housing data to keep you well-informed about what’s going on in the real estate market.

Hello there, I’m Windermere’s Chief Economist Matthew Gardner and welcome to this month’s episode of Monday with Matthew.

If you’ve listened to me at all over the past several years, you’ll know that I am pretty passionate about one subject: housing affordability. And, given the significant price growth that we’ve seen over the past decade, as well as the recent spike in mortgage rates, I wanted to talk a little bit about what might be done to address this very serious issue.

The Growing Housing Affordability Problem

Now, when we think about housing affordability and how it might be solved, a lot of people get tied up in the minutiae when, quite frankly, it really isn’t that hard a problem to solve. You see, there’s one very simple way to address this: to build more housing units. But, as easy as that may sound, there are a lot of obstacles that are holding new supply back. But before I get to that, I want to share some data with you that might help to demonstrate how serious an issue we all face.

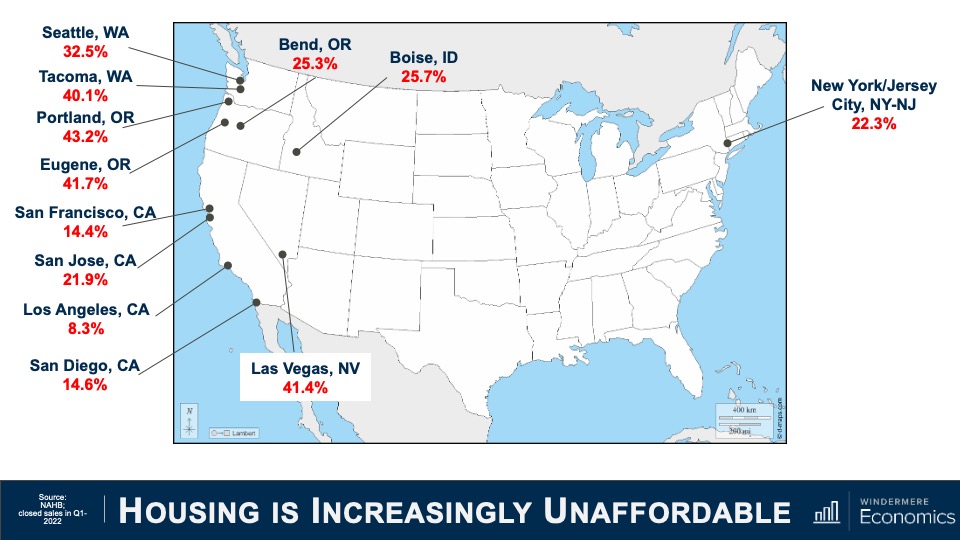

Every quarter, the National Association of Homebuilders puts out its affordability numbers for metro areas across the country. An analysis of sales and incomes allows them to show the number of homes—both new and existing—sold in a quarter that were affordable to households making median income.

Housing is Increasingly Unaffordable

Here you will see numbers from just a few of the 240 metropolitan areas across the country and the share of sales in the first quarter of this year that were “technically” affordable. I think you’ll agree that it’s eye opening.

Although I am only showing you a few of the U.S. markets I will tell you that the ten least affordable US housing markets were all in California. The Golden State is also home to 21 of the top 25 least affordable markets in the country. But what you might also find interesting is that our primary cities aren’t the only ones that are suffering from affordability issues, with markets like Bend, Oregon; Boise, Idaho; and even Las Vegas, Nevada becoming increasingly unaffordable for a lot of households.

And it’s worth mentioning that that 48 of the 69 markets where less than half of the homes sold were affordable were in states that have at some point in the past implemented comprehensive planning and growth management legislation. And when governments mandate where homes can and cannot be built, one thing happens: it pushes land prices higher which makes new homes more expensive and limits the amount of new supply that builders are able to provide. So, what can be done?

Well, I will start out by saying that states who have implemented growth management plans, which they generally did to slow or stop suburban sprawl, remain disinclined to move these boundaries, and that means it becomes paramount to not look further out but to concentrate within the urban growth boundaries and decide whether it’s time to think about removing single-family zoning altogether.

This is a fascinating thought, but I must add that I am not suggesting that we do away with single-family homes. Absolutely not! What I am thinking about is the ability for a market to decide what makes the most sense. In order to do so, single-family zones need to allow for the development of denser housing, but also allow the market to decide what’s best. Areas that have implemented such change has given rise to a movement in order to address what is being referred to as “missing middle housing.” For those of you who are unfamiliar with this term let me try and explain.

Missing Middle Housing

This is a great image courtesy of Opticos, a team of urban designers, architects, and strategists who are passionate about adding sorely needed housing options.

They came up with the term “missing middle” as it describes housing types that were actually very common prior to World War II where duplexes, row-homes, and courtyard apartments were in high demand. Unfortunately, however, they are now far less common and, therefore, “missing.”

And the key function of this type of housing is to meet the rising demand for walkable neighborhoods, respond to changing demographics, and provide housing at different price points. You see, rather than focusing on the number of units in a structure—think high rise apartments or condominiums—this type of housing emphasizes scale and heights that are appropriate for and sympathetic to single-family or transitional neighborhoods.

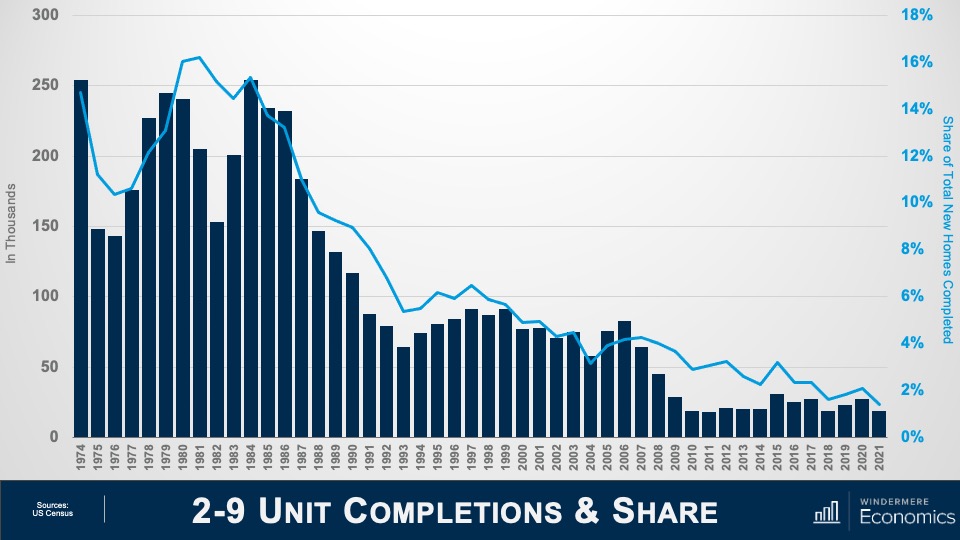

The Decline of Missing Middle Housing Construction

And to show you how supply of these types of units has changed, this chart shows the number of duplexes to eight-unit buildings built over the past almost half-century and you can clearly see that up until the late 1980s they were being built in decent numbers, but the 1990s saw a significant shift toward traditional single-family home ownership and builders followed the demand and this type of product started to become scarcer.

Almost 16% of total new homes built in America in the early 1980s were of this style, but that number has now shrunk to just 1.4%—or a paltry 19,000 units.

But I see demand for these housing types growing as we move forward and that buyers or renters, young and old, will be attracted as it will meet their requirements not only in regards to the type of home they would want to live in but, more importantly, it can be built cheaper than traditional single-family housing and therefore it will be more affordable.

But although this sounds like it’s a remarkably simple solution that can solve all our woes, in reality it’s not that easy for two very specific reasons. The first is that many markets are already essentially built out, meaning that in order to develop this type of product, a builder would have to purchase a number of existing homes and raze them in order to rebuild. But given current home values, it’s very hard for a builder to be able to make such a proposal financially.

And the second issue is that current residents within these “transition” areas—which have been developed as traditional single-family neighborhood—simply don’t want to see change. But is this type of product bad? Here are some examples.

This shows row-homes in Brooklyn on the left and traditional “triple-deckers” in Massachusetts on the right:

This is a bungalow court project in California:

Here are some Live/Work Units in Colorado:

These are some amazing mews homes in Utah:

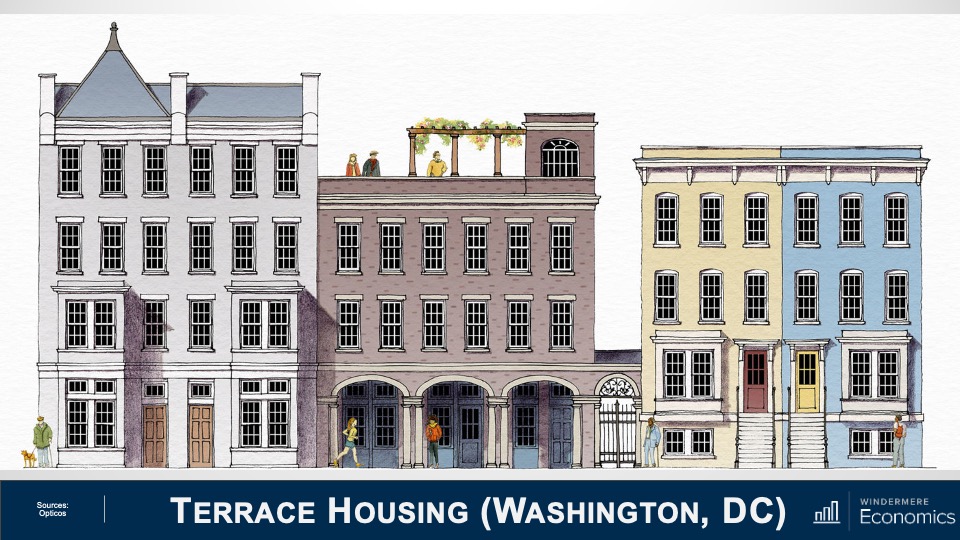

And finally, a new terrace housing project that will be built in Washington DC:

Don’t get me wrong, I’m sure that some of you who simply aren’t inspired by this type of architecture, and that is understandable. But can we simply stick with the status-quo? I don’t think so. And some state legislators have already implemented significant zoning amendments in order to try and encourage this type of development.

Back in 2018, Minneapolis was the first city to allow this type of development inside single-family zoned areas. This was followed by Oregon State in 2019. Senate Bill 9 was signed by Governor Newsom of California last year which made it legal for property owners to subdivide lots into two parcels and turn single-family homes into duplexes, effectively legalizing fourplexes on land previously reserved for single-family homes. So, we are starting to see some change.

This is a good start but as I mentioned earlier in areas that are already built out, even this type of forward-thinking legislation will not be the panacea that some want. But I’m not giving up hope.

Addressing the “missing middle housing” would allow for homes of all shapes and sizes, for people of all incomes including workers who are essential to our economy and community. Here I am talking about our teachers, firefighters, administrative assistants, childcare providers, and nurses—just to name a few!

There are currently 45 million Americans aged between 25 and 34 and most aspire to homeownership. However, the massive price growth which, by the way, many of us have benefitted from over the past several years, has simply put a “starter home” out of their reach.

I will leave you with one last statistic. Over 28% of American households today are made up of a single people living alone, and it is anticipated that up to 85% of all U.S. households will not include children by the year 2025. Finally, by 2030, one in five Americans will be over the age of 65.

Are we going to meet the needs of the country’s changing demographic going forward? I certainly hope so, but it will take a lot of work for us to get there. As always, if you have any questions or comments about this particular topic, please do reach out to me but, in the meantime, stay safe out there and I look forward to visiting with you all again next month.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link