Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

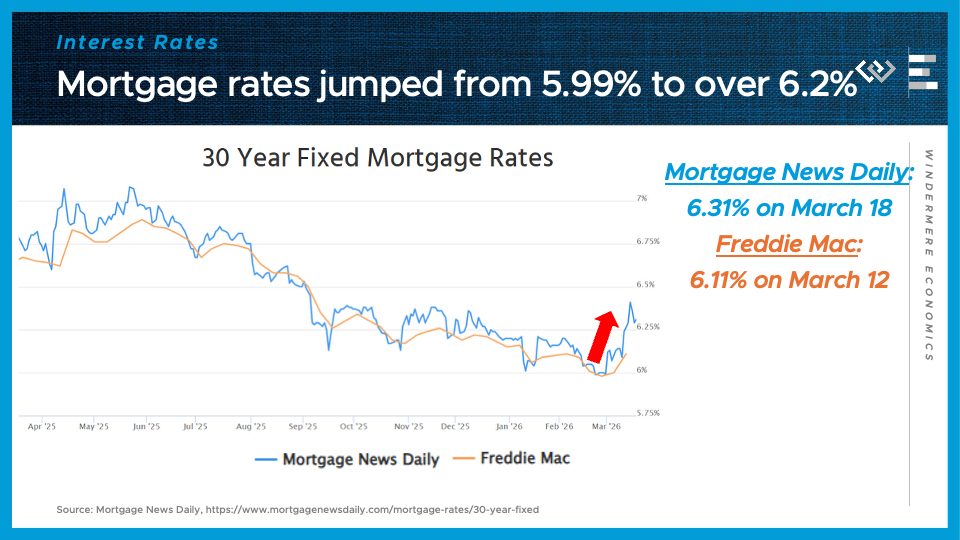

King County homebuyers are increasingly turning to adjustable-rate mortgages to reduce their monthly homeownership costs. With the county’s median home price approaching $1 million and mortgage rates stubbornly above 6%, the affordability pressures driving this trend continue to grow.

Unlike traditional fixed-rate mortgages, adjustable-rate mortgages start with a lower interest rate that remains fixed for an initial period of several years before adjusting with the market. That lower starting rate is the primary draw for buyers looking to reduce their monthly payments.

In 2025, 36% of King County home purchases involved an adjustable-rate mortgage. Across Washington, adjustable-rate mortgages made up nearly a quarter of home loans, the highest share the state has seen since 2007. With mortgage rates on the rise again due to inflationary and political pressures, and no Federal Reserve cuts expected, experts say that share is likely to keep climbing.

Adjustable-rate mortgages are typically 0.5% to 1% lower than conventional fixed-rate mortgages, totaling a minimum savings of roughly $244 per month on a $750,000 loan at today’s rate. In King County, where prices routinely exceed that figure, the savings can be even more significant.

Many buyers are betting that rates will fall before their fixed period ends, allowing them to refinance, or plan to sell before their rate adjusts at all. Industry experts describe it as a relatively low-risk approach for buyers who do not expect to stay in their home beyond the typical seven-year window.

Adjustable-rate mortgages carry a stigma from the 2008 financial crisis, when they played a central role in a wave of foreclosures. Lenders at the time offered extremely low introductory rates lasting only two or three years and approved practically anyone regardless of their ability to repay. By 2004, these loans made up half of all home loans in Washington. When borrowers could not afford the higher rates, the fallout reshaped the housing market for years.

Today’s adjustable-rate mortgages are a different product entirely. Lenders must now verify that borrowers can afford the loan at higher post-introductory rates, initial fixed periods are longer, and rate discounts are more modest, making the kind of payment shock that defined the 2008 crisis far less likely.

With ongoing affordability concerns statewide and across King County, adjustable-rate mortgages offer a way to reduce the initial cost of the loan. In large part, their increasing popularity stems from the growing gap between home prices and what many borrowers can afford.

This post was based on information found on Puget Sound Business Journal.