There is perhaps no other home décor style as comforting as traditional interior design. Rooted in the masterfully crafted Chippendale and Thomas Sheraton furniture designs and classic Queen Anne colors, traditional décor is one vintage style that stood the test of time. Here are five distinct features of traditional interior design.

5 Features of Traditional Interior Design

1. Dark Wood Finishes

Part of the reason for traditional design’s timeless appeal is its use of woodworking. With woodwork as a foundation, this design style feels classic but not dated. The dark, bold colors resemble the Victorian style, but traditional interiors are simpler and less ornate. The dark tones of the wood create a foundation for a more colorful decorative palette.

Traditional interior design living room with dark wood finishes | Image Source: Getty Images – Image Credit: IPGGutenbergUKLtd

2. Traditional Design Color Palette

Traditional design can handle a heavier color palette while still providing comfort. The darker wood tones allow for darker color to be used elsewhere throughout a space, such as dark window coverings. Floral, plain colors, and muted plaids are all common color schemes. Walls are often covered with patterned wallpaper, floral designs, or damask. In terms of designs, traditional interiors pair well with geometrics and small, striking yet understated patterns.

3. Hardwood Flooring

This design style is classic from the floor to the ceiling. You won’t find laminate or tile flooring in the common areas of a home that adheres to the principles of traditional interior design. Complimenting the surrounding woodwork, homes designed in this style have solid hardwood flooring. How to Choose the Best Flooring

Traditional interior design living room with hardwood flooring | Image Source: Getty Images – Image Credit: mikolajn

4. Traditional Decorations

The decorations used in traditional design help to reinforce its unique, classic-yet-comfortable ambiance. Table lamps and vases are typical of a traditional interior, often displayed in pairs to create symmetry. Though these accessories are bold, they are never too ornate or over-the-top enough to dominate the room.

5. Design Philosophy

Traditional design is calm and orderly. Whereas a more eclectic interior design style may offer more surprises throughout its spaces, a traditional interior is more predictable. Even the textiles used are subtle, with typical materials ranging from cotton and fur to velvet and silk.

For more inspiration and interior design tips, visit the Design category of our blog:

Maintaining a tidy home not only helps it to look its best, but it also makes for a more peaceful and organized living environment. Regardless of the size of your home, these tips will help you achieve and maintain a consistently tidy and inviting living space that you, your household, and your guests will enjoy. With a few simple steps, you can go from cluttered to tidy in no time.

5 Tips for a Tidy Home

1. Start by Decluttering

The first step on your journey to tidiness is getting rid of clutter lying around your home. Go through each room and evaluate your belongings, asking yourself what is truly necessary among them. If something isn’t a keeper, consider donating, selling, or discarding it. Decluttering creates more spaces and will make cleaning up easier in the long run. Not sure where to start? Focus your initial decluttering efforts on the closets throughout your home and see how much space you can open up for belongings that are currently stored elsewhere.

Making your home tidy is one thing; keeping your home tidy is another. The difference between the two is finding and establishing a cleaning routine that works for you, whether that means doing a few upkeep chores daily or hit “reset” by dedicating a chunk of time to it once a week. Whatever you choose, consistency is key. Include quick tasks like making the bed, wiping down kitchen counters, and doing a load of laundry. Having a routine in place will help you keep up the momentum that’s required to maintain a tidy home.

Everything in your home has to go somewhere. To stay organized, store your items neatly in dedicated bins to maximize your storage efficiency. Keeping items accessible but stored out of sight will give you more room in the open areas of your home and help each room feel tidier. Use containers, shelves, and organizers to keep items like toys, books, and accessories neatly arranged. In the closet, you can maximize space by using hangers, bins, and dividers to keep your wardrobe and accessories in order.

4. Multi-Purpose Cleaning Products

Using multi-purpose cleaning products will simplify your cleaning process and get your home sparkling clean. Having a single cleaner to tackle tough stains and messes around the house can save you money too. Natural cleaning solutions that you can find in the aisles of your grocery store will streamline your cleaning efforts without spraying chemicals throughout the house. Things like lemons, salt, and vinegar will eliminate household odors and can even help to keep bugs and pests at bay. When shopping for cleaning products, look for organic solutions that won’t harm members of your household and your pets.

Turn your attention to high-traffic areas throughout the house such as the living room and the kitchen. Improvements in your home’s tidiness in these areas will go a long way in contributing to its overall cleanliness. Also, focus on cleaning your appliances. These machines are the workhorses behind a well-functioning home, so giving them some attention will help keep things tidy at home in the long run.

As you start searching for homes, you’ll likely come across different terms that describe the status of different listings. One term, “Days on Market” (DOM), can play a role in your strategy for making an offer. Knowing what this term means will help to inform your discussions with your agent as you go about finding the right home for you.

What is Days on Market (DOM)?

Days on Market (DOM) is a metric used by real estate professionals (and home buyers) to measure the time that a certain property has been listed for sale. In other words, it’s the running total number of days since a home hit the market. Different factors contribute to how long a home is on the market, including the home’s features, its location, and the local market conditions. Brush up on seller’s and buyer’s markets to understand how these market conditions affect days on market.

Buyer Hesitancy: Just like contingent and pending listings, a home with a longer Days on Market may make buyers think there is something wrong with the property. The right buyer may very well come along, not swayed in their decision by the DOM number, but for some, it raises questions about why the home hasn’t sold yet.

Market Value: Over time, Days on Market can impact the home’s listing price and how much it ultimately sells for. If a property stays on the market for an extended period, the seller may need to reduce the price to prevent it from going stale. On the other hand, the longer the DOM, the more leverage a buyer potentially has to negotiate a more favorable offer.

Local Market Conditions: Looking at trends in DOM can give both buyers and sellers a better understanding of local market conditions. If homes are flying off the market left and right with low DOM, it’s a competitive market that favors sellers. Buyers will be more likely to remove contingencies to make their offer stand out amongst the competition. If DOM is high across the board, the market is not as competitive, and buyers have more leverage.

Negotiations: The leverage created by Days on Market flows through to negotiations. If you have leverage on your side, you can expect that the seller will be more willing to negotiate on price or repairs than they would if the tables were turned. Make sure you and your agent are on the same page regarding how the DOM figures you’re seeing locally will affect your strategy for making an offer on a house.

Talk to your real estate agent for more information about Days on Market (DOM) and how long homes are staying on the market near you. This one statistic could alter your strategy for approaching the market and, when the time comes, how you put together your offer on a home. Connect with an experienced Windermere Real Estate agent today to learn more:

The desire to maximize property value among homeowners is stronger now than ever. As the movement of short-term rentals, turnkey properties, and real estate investment continue to grow in popularity, it’s worth it to take a moment and understand the regulations that dictate a property’s potential. Understanding a bit more about the process for obtaining the necessary permits to build structures on your property will help you avoid getting bogged down in legalities when trying to complete these projects.

Do I need a permit to build an ADU?

Accessory Dwelling Units (ADUs) and other additional property structures have emerged as viable options for homeowners looking to maximize their property’s potential. These structures offer additional living space while creating opportunities to generate extra income or accommodate multigenerational family members. But before you break ground on your building project, here are some of the things you should keep in mind.

Permits and Regulations: No matter where you live, it is necessary to obtain the appropriate permit before you begin the construction process. Permits ensure that your project complies with local building codes and regulations. Though some guidelines are universal, keep in mind that every local area has its own specific building requirements for residential properties.

Code Compliance: Building codes aren’t just red tape for the sake of red tape; they exist to make sure that all buildings are safe. Whether you’re building the structures on your property DIY or hiring a professional to do the job, you are the one kickstarting the project, not your local municipality. But by having these codes in place, they can ensure that you’re adhering to the required standards of safety. Before you even start on your project, familiarize yourself with your local codes and regulations. Contact your local zoning department or building authority to learn more.

Applying for a Permit: The permit application process varies by location. Typically, you’re required to submit detailed plans for your project with documents that outline its scope, size, etc. Whether you submit architectural drawings, engineering plans, or some other form of detailed blueprint, be prepared for a thorough review on behalf of your local authority to make sure your project complies with the rules.

Whatever project you have in mind—ADU, garden shed, pool house—it’s important to become well-versed in the permits and regulations that will allow you to get it built hassle-free. Consult with local authorities to get the full picture of what’s required from you. Once you’ve checked all the boxes, you’ll be well on your way to maximizing the value of your property. Pair your building project with these design ideas to take your backyard to the next level:

Buying a home is one of the most significant financial and emotional purchases of a person’s life. That’s why it is so important to find an agent that can not only help you navigate the home search process while answering your questions and addressing your needs from start to finish. Most importantly, your agent should care about your happiness and ensuring that you find the right home for you. Here are some important qualities to consider when selecting a real estate agent.

10 Qualities to Look for in Your Real Estate Agent

1. Likable: More than likely, you will be spending significant time with your agent. You’ll be side by side throughout the ups and downs of the buying process, so it’s worth it to spend time looking for someone that you enjoy interacting with. Working with a Buyer’s Agent

2. Trustworthy: One of the best ways to find an agent who you feel you can trust is to ask friends and family for a referral. You can also interview different agents and ask for client references. When vetting agents, prioritize their trustworthiness along with their business acumen and ask questions that will help you narrow your search. If you’re having trouble knowing where to begin. Here are a few common questions you can ask to get the conversation started:

How do you help buyers to make their offer stand out?

How many clients are you working with currently?

What is the best way to contact you?

How long have you been an agent in the local market?

Do you represent both buyers and sellers?

Do you have recommendations for mortgage brokers, home inspectors, etc.?

3. Effective Listener: While your agent can’t read your mind, they should be able to make educated recommendations and offer advice by listening closely to your needs. Make sure you talk to your agent about your priorities, what types of features appeal to you, as well as any factors that could be deal breakers. This will equip your agent with everything they need to help find you the perfect home as they explore the Multiple Listing Service (MLS) for available listings.

4. Qualified and Experienced: Make sure your agent has the qualifications and experience to meet your specific needs. For example, some agents have more experience with short sales, while others might be experts on certain neighborhoods or types of housing. Find someone who is good at what you’re looking for. Ask specific questions when you interview them so you can get a better idea of what they’re great at, and if they’ll be a good fit for your search. For a comprehensive list of real estate agent certifications, visit our blog:

5. Knowledgeable: A great agent is someone who is out in the neighborhoods, exploring communities, visiting listings, staying up to date with market and industry news, and collecting all the information that you need to make an informed, confident decision about your real estate needs. For up-to-date information about your local market, visit the Market News category of our blog.

6. Honest: Your agent should be upfront and honest with you about every aspect of your home search process—even if it involves delivering bad news. The best real estate agents are more concerned about finding the right home for their clients, not just the home that brings in the fastest commission check.

7. Local: Every community is different, and all real estate is local, so it’s important to find someone who really knows the local market and can provide you with the information you need to familiarize yourself with a particular area. This will narrow your home search and help you find listings you can afford.

8. Connected: A well-connected agent will have relationships with lenders, inspectors, appraisers, contractors, and any other service provider you might need during your home search. Though your agent will be your greatest asset in the home buying process, it takes several people to successfully purchase a home.

9. Straightforward: You want an agent who will work hard to help you find the best home, but you also want someone who will be straightforward with you about the process and how to set realistic expectations given the market conditions in which you’ll be buying.

10. Committed: Your agent should be in it for the long haul, meaning that they’re looking out for your best interests every step of the way, no matter how long the process takes. Connect with a local, experienced Windermere Real Estate Agent today:

Your home’s interior can offer you peace of mind, but there’s nothing like the connection between your patio and the great outdoors. With a little privacy, you can relax and unwind at home like never before. Here are five creative tips to add privacy to your patio or balcony and turn into your own personal retreat.

5 Ways to Add Privacy to Your Patio or Balcony

1. Vertical Gardening

Incorporating nature into your outdoor space will not only help you make it more private, but it will also help bring the space to life with an organic touch. Vertical gardens will liven up your patio while making it more secluded. Choose plants that thrive in your local climate and complement your home décor style.

2. Install a Pergola or Canopy

Looking to make your backyard a bit more exclusive while providing some shade? A pergola or canopy will do the trick. This versatile choice is also fitting for any homeowners who like to entertain and want to extend their parties to the outdoors. To set up, pick a central space on your patio for your pergola that won’t interrupt the flow of foot traffic. These furnishings may be the missing piece for your backyard retreat; they will protect you from the elements year-round while maintaining that open-air feeling you’re looking for.

Your patio privacy project will lead you toward some creative decorative opportunities. Privacy screens work like a fence for your home, in that they help to enclose your property from your neighbors. However, unlike a fence, they are easy to move around and come in various styles and materials to match your taste in outdoor décor. Typically made of vinyl, metal, wood (bamboo is a popular choice), and artificial greenery, these products may be just what you’re looking for to frame your private patio area.

4. Planters

You can create a barrier and refresh your backyard or balcony patio aesthetics at the same time with planters filled with tall plants. If you’re willing to wait, trees and vining plants can grow into lush fences over time. If you’re hoping for a quicker solution, consider lifted planters with mature bushes or hang planters with plants that cascade down. How to Create a Balcony Garden

Image Source: Getty Images – Image Credit: vm

5. Outdoor Curtains and Art

Finding the right items to hang will help create the backyard oasis you’re dreaming of. For those with a vertical structure in the backyard like a pergola or gazebo, or a balcony that can hold a tension rod, consider adding outdoor curtains for some elegance and privacy. For a more personalize approach, a gallery wall can also help keep the creative juices flowing outdoors while connecting the space to the inside of the house. Search for weather-resistant frames that will hold up as the seasons change and hang them on sturdy strings or repurpose a room divider. How to Create a Gallery Wall at Home

With a dash of décor, some elements of nature, and your own personal design touch, you’ll create the outdoor space you’ve always wanted. No matter how much we love our interior, it’s nice to get outside and breathe some fresh air while still feeling like you’re at home. Get more tips on how to transform your home here:

Nothing beats the feeling of buying a new home. You’ve worked hard with your agent to find the right home for you, you’ve worked with the seller to finalize the deal, and you’ve signed all the paperwork to transfer ownership. Congratulations! Everything has led to securing your new home, so now that you’re officially moving, what do you do next? Here’s a quick guide to the move-in process to help you get settled into your new home.

Moving Day

The day you move, you’ll be juggling all kinds of timelines at once. You’re coordinating with movers, arranging for trucks to be picked up and dropped off, and making sure that nothing gets damaged in the process. The best thing you can do on this chaotic but exciting day is to be available. Being on hand at your new home to answer the mover’s questions will help speed up the process.

It helps to have a checklist of your important items to make sure nothing has gotten lost during the moving process. Check these items off one by one as the movers bring them in. Next, you’ll want to confirm that the utilities have been turned on and are ready for use. Check all lights, smoke detectors, appliances, CO2 alarms, your home security system, fire extinguishers, etc. Finally, install new locks and make sure your keys work properly.

Clean and Unpack: Before you start emptying your boxes, it’s a good idea to wipe down the surfaces to keep your items from getting dirty. A full deep cleaning of your home may not be in the cards just yet since there’s still plenty of moving to be done, which inevitably brings more dust and dirt in the house.

Childproof and Pet-Safe Home: If you’ve got little ones and/or pets, this is the time to set up their accommodations. Learn more about how to properly childproof your home so your kids can feel like it’s home sweet home from day one. When preparing to house your pets, keep in mind that some cleaning methods are more pet-friendly than others.

Setup and Organize: Now it’s time to get everything in its right place. Organize room by room, storing items in logical places where you won’t forget them as soon as they’re stowed away. The first rooms you’ll want to tackle are the bedrooms, bathrooms, and kitchen. These are the rooms you’ll need the most during the first few days in your new home, so having them put together will better position you to tackle the rest of the house. Getting your closets, bathroom cabinets, and kitchen drawers organized from the start will make for a more enjoyable moving process.

Update Your Information: You’ll also want to update your address everywhere it’s applicable as soon as possible, consider setting up mail forwarding to ensure you don’t miss any important mail in the meantime.

For more information on the moving process, visit our comprehensive Moving Checklist, available as a interactive webpage and downloadable PDF here:

Sold for: $823,000

Listed for: $789,000

Sold for 4.3% over asking

Beds: 4

Baths: 4

Size: 2,900 sqft

Days on OneHome: 6

Dream location! Well-designed home tucked on quiet culdesac across from Lk Meridian. Custom built with advanced systems and thoughtful extras for hi performance living & entertaining: Soaring 2story foyer entry, open flr plan, luxury plank flooring, professional Chef’s kitch, 4 skylites, gas frplc, 2 Primary bedrm suites, 4 bths. Kitchen is center stage w/custom cabinets, Dacor double convection ovens, Viking 6 burner gas range/hood with heat lamps, wine cooler & 2 pantries. Main flr Primary suite has luxury spa bath, jetted soaking tub, roll-in shower. Huge 740sqft. garage, wired for generator. All bordered by lush Soos Creek Trail forests, an ideal chance for vacation lifestyle just min. from necessary freeways & shopping centers.

10115 SE 207th Street Kent, WA 98031

Sold for: $750,000

Listed for: $650,000

Sold for 15.4% over asking

Beds: 3

Baths: 3

Size: 1,620 sqft

Days on OneHome: 4

Stunning MidCenturyModern daylite rambler in exceptional private setting. Custom designed/built one-owner home, enchanting woodland lot, refined spaces w/top quality MCM finishes in pristine condition. Great floor plan! Formal liv rm, updated quartz & tile kitch w/family rm, 3 firplc, lots of windows & glass doors open to light, sky & the great outdoors, views from every room. Big deck for entertaining, updated privt bath off Primary bedrm. Walk-out basmt is a clear slate for finishing your way: 4th bath plumbed, more bedrms, recrm, etc. Huge workshop w/sep entry is already there. All this space, peace & quiet just min. to freeways, shops, Kent Station, SeaTac Airport, & more. A rare chance to own a uniquely personal, distinctive estate.

Helped Buyer Get Under Contract

5239 39th Avenue S #B Seattle, WA 98118

Sold for: $899,000

Beds: 3

Baths: 3

Size: 1,550 sqft

Days on OneHome: 27

Lovely stand-alone townhome with no shared walls, close to the heart of Columbia City w/all the shopping, restaurants, and library walking distance. Looks over lush greenery of city owned land. Lots of privacy between the 3 lg bdrms, each w/their own baths plus half bath on main floor, and a stunning open kitchen and dining area w/lots of natural light from the large windows. Enjoy the outdoors on all three floors w/2 decks and patio area. One car garage with some storage. Built-Green 4 Star & Energy Star Certified by 3rd party verifier

Windermere Chief Economist Matthew Gardner gives an updated look at U.S. home prices and housing affordability in 2023 by examining two key second-quarter reports from ATTOM Data Solutions and the National Association of Home Builders (NAHB).

This video is the latest in our Monday with Matthew series with Windermere Chief Economist Matthew Gardner. Each month, he analyzes the most up-to-date U.S. housing data to keep you well-informed about what’s going on in the real estate market.

U.S. Home Prices 2023

Hello there, I’m Windermere Real Estate’s Chief Economist Matthew Gardner and welcome to this month’s episode of Monday with Matthew. Today we are going to look at home prices and housing affordability. To do this I will be looking at the second quarter sales price data from ATTOM Data Solutions and we will also look at the just released National Association of Home Builders Housing Opportunity Index for the second quarter.

Are home prices dropping?

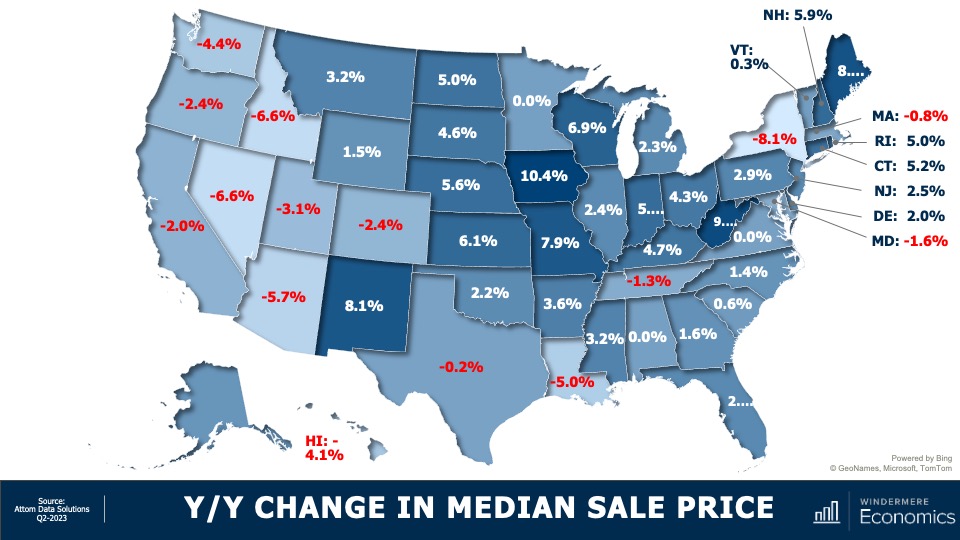

Starting with the year-over-year change in sale prices at the state level, there aren’t any great surprises. For the past several months I’ve been saying that as the Western U.S. saw the greatest price growth during the pandemic, so it’s not surprising to see most states sale prices in the quarter below the level seen a year ago. But it was pleasing to see that sale prices in 36 states either matched the level seen a year ago or were higher, and in some instances quite significantly so.

U.S. Home Sale Prices 2023 By State

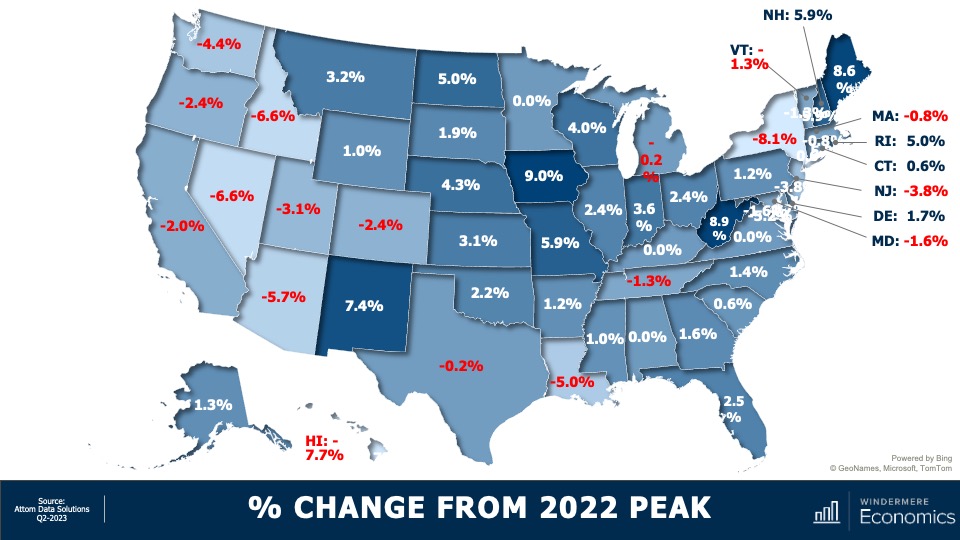

And when we compare second quarter sale prices to their 2022 peaks, 33 states are at or above the highs seen last year, but most of the Western States have yet to fully recover. In the South, Louisiana is still lagging by a good amount, as is New York State on the East Coast.

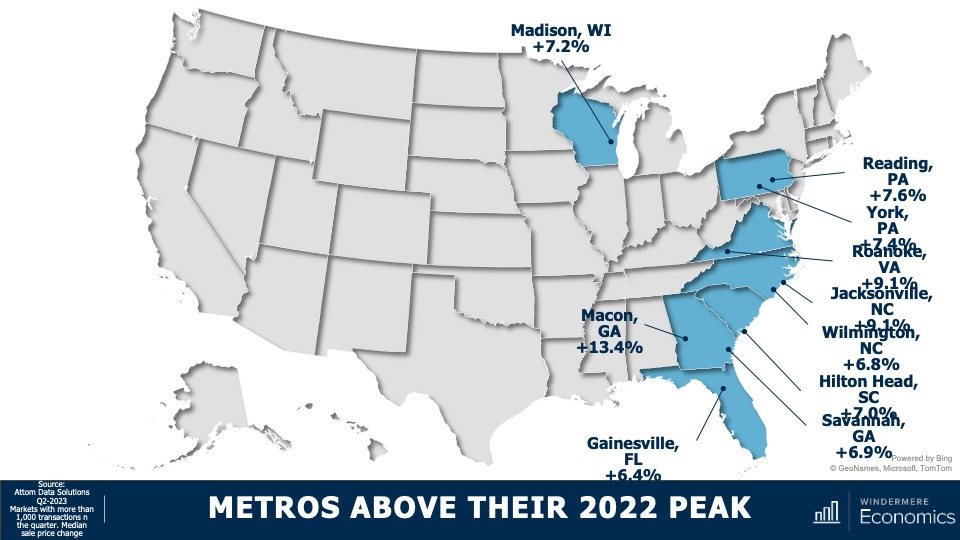

But as you are all very aware, all markets are different. I thought it would be interesting to dig a little deeper into the data to see which metro markets have seen significant gains over the past 12 months. It’s going to be interesting specifically because of the fact that mortgage rates have risen so much.

Metro Areas: Home Sale Prices 2023

These are markets where sale prices are far above their 2022 peak sale prices. Now I must add that I only looked at markets where more than 1,000 transactions occurred in the last quarter, which takes out some of the volatility. Notably, even though the state of Virginia’s home prices in the quarter were flat when compared to their 2022 peak, the Roanoke market was up by over 9%. And in Pennsylvania, where state prices were only 1.2% above their 2022 peak, Reading is up by 7.6% and York by 7.4%. And in Georgia, where state sale prices were up a modest 1.6%, homes in Macon have leapt by over 13% and prices are up by 6.9% in Savannah.

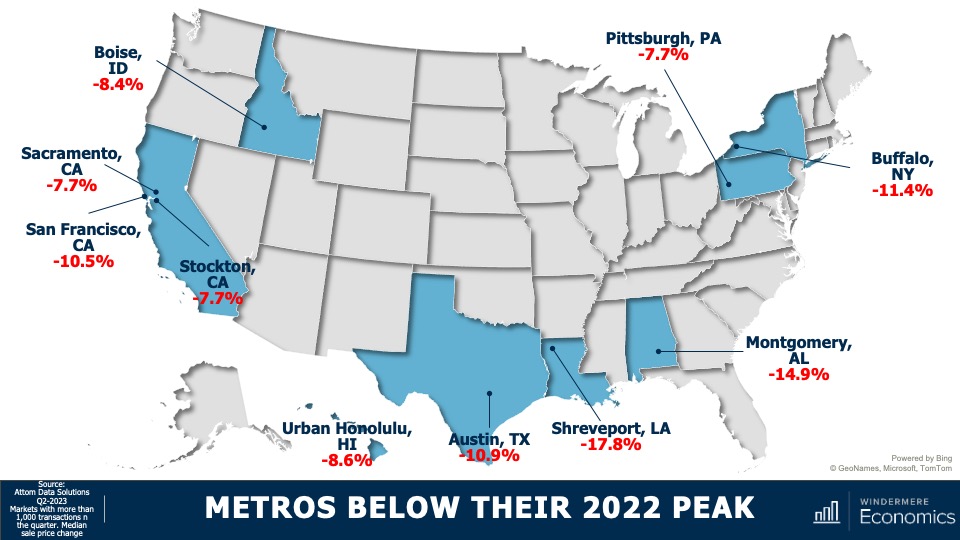

But, on the other end of the spectrum, there are markets which are underperforming their respective states and, unsurprisingly, California tops the list with three of their metros seeing prices significantly below that of the state as a whole. In other parts of the country, several metro areas which were relatively affordable before the pandemic saw an influx of remote workers and this led prices to skyrocket, and these will take some time to recover. This is particularly true in the Austin and Boise market areas.

I would add that, of the counties across the country where there were more than 1,000 transactions in the second quarter, half have met or exceeded their prior peak and—of the half where sale prices were still lower—the average shortfall is only around 4% and there are just seven counties in the country where sale prices are down by more than 10% from their 2022 peaks.

Now, what I see in the data is that the U.S. housing market, although certainly not fully healed, is headed in the right direction even when faced with mortgage rates that remain remarkably high. So, with sale prices recovering and still faced with stubbornly high financing costs, what does affordability look like?

U.S. Housing Affordability 2023

Well, according to the National Association of Homebuilders (NAHB), of the 241 metros that they track, just 40.5% of sales in the second quarter were affordable to households making the area’s median income—that’s the second lowest share of sales seen since they started generating this dataset a decade ago. Now, their data does go back to 2004, but the interest rate series that they used to use was discontinued, so it’s not accurate to compare their data today with anything before 2012.

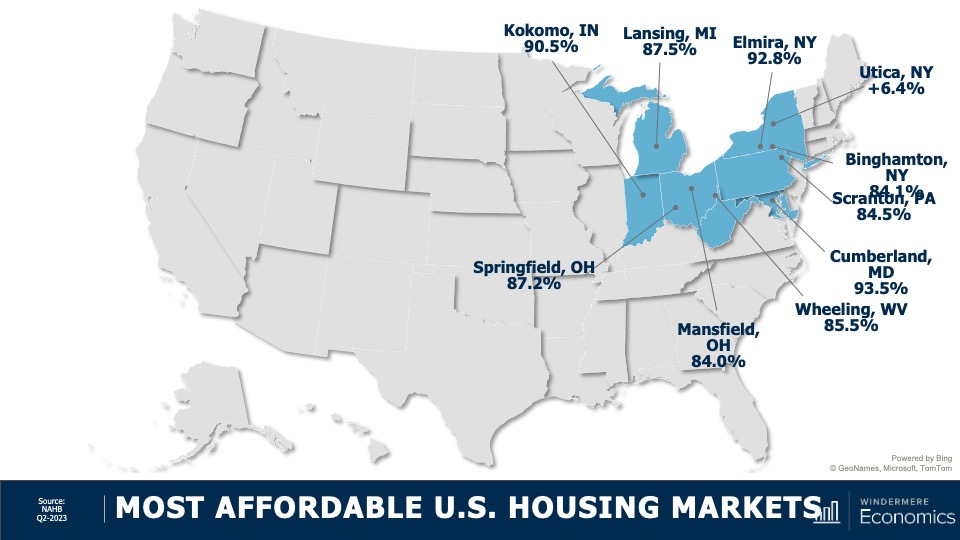

Most Affordable U.S. Housing Markets

These were the most affordable markets in the second quarter and their locations should not be of any great surprise. Average sale prices in these markets were measured around $203,000—that’s just marginally above 50% of the national sale price in the quarter, which was $402,600.

Least Affordable U.S. Housing Markets

And unfortunately this should not surprise you either. On the other end of the spectrum, the top-10 least affordable housing markets were all in California, but it gets worse than that. The top 15 least affordable markets again, all in California, and 19 out of the top 25 were in the Golden State!

As far as I can see, the ownership housing market is still showing remarkable resiliency, especially given that mortgage rates have more than doubled from their lows and they’ve risen from 4.8% at the start of the second quarter of last year to 7% at the end of the second quarter of 2023.

Now, I still expect to see rates starting to slowly move lower as we go through the second half of the year. This will help with prices and, to a degree, affordability, but until we see a significant increase in the number of homes listed for sale, the market is going to remain unbalanced.

As always, I’d love to hear your thoughts on this subject so feel free to leave your comments below. Until next month, stay safe out there and I’ll see you soon. Bye now.

To see the latest real estate market data for your area, visit our quarterly Market Updates page.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Whether you’ve listed multiple homes or you’re a first-time home seller, you’ve likely come across the word “contingent” before. Contingent home sales, though very common, aren’t as simple as a real estate transaction without them. With contingencies, there are additional factors at play and added criteria that need to be met for the deal to go through. As a seller, being aware of these offers will help to inform your discussions with your agent once you know it’s time to sell your home.

What is a contingent offer?

Contingent offers in real estate give the buyer or seller the right to back out of the contract if the conditions aren’t met. There are different types of contingencies that determine what must happen for the deal to go through, which means buyers have options. Depending on their situation, whether they are selling their current home while making an offer on yours, unsure whether they can secure the right financing, or want to wait for the results of the home inspection before finalizing their offer, they’ll explore contingencies with their real estate agent as they build their offer.

This may feel a bit like buyers want to have their cake and eat it too, but every homeowner can understand the desire to protect their investment before fully diving in. In a seller’s market, there are fewer homes available, which means buyers will do whatever they can to make their offer stand out. Because sellers have the leverage in these market conditions, you’ll often see buyers waiving their contingencies. Talk to your agent for more information about the local market conditions in which you’re selling.

Should I accept a contingent offer on my house?

Each home sale is different, and each seller has a unique story. What you’re looking for in an offer may be different from what someone else in your neighborhood is looking for when selling their home. It all depends on your circumstances, your timeline, your next steps, and your local market conditions. The extra stipulations in a contingent offer require the attention of an experienced real estate agent who can interpret what they mean for you as you head into negotiations.

Contingent offers can fall through more often than non-contingent ones, but there’s no general rule of thumb. Whether a sellers and buyer are able to agree on the terms of a deal is a case-by-case situation. Different contingencies may carry different weight among certain sellers, and local market conditions usually play a significant role. For up-to-date information about your local market, visit the Market News category of our blog.

Pros: Accepting a contingent offer means you don’t have to take your home off the market quite yet, since the conditions of the deal haven’t been met. If the buyer backs out of the deal, you can sell without having to re-list. In certain cases, some buyers may be willing to pay extra to have their contingent offer met.

Cons: Home sales with contingent offers are usually slower than those without. It takes time to satisfy a buyer’s contingencies and additional time to communicate that they have been met. And of course, there’s always the risk that the deal could fall through.

As always, trust your agent for guidance when facing contingent offers. Connect with a local Windermere Real Estate agent today:

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

14816 SE 267th Street

14816 SE 267th Street  10115 SE 207th Street

10115 SE 207th Street  5239 39th Avenue S #B

5239 39th Avenue S #B